Purchasing a multifamily property can be a great business opportunity, but the process can be complex and should be managed by experts. You can count on the highly experienced team at LSG Lending Advisors to help you execute a successful multifamily finance transaction. Regardless of whether your goal involves a purchase, acquisition, or refinance, our team is here to help. We offer the finest multifamily property financing services in the industry.

- Over 7 years multifamily property loan underwriting experience.

- Expert knowledge of financial terms and principles.

- Highly experienced at guiding clients through complex transactions.

- In depth analysis of current operating statements and projected financials.

- Specialists in evaluating third party reports, including appraisals, environmental documents, market studies and project capital needs assessments.

- Loan review documentation.

- Tailor fit financing solutions for every client.

Our extremely knowledgeable professionals have many years of experience in evaluating both current and future multifamily projects for compliance with FHA/HUD MAP lending guidelines. We can also put you in contact with some of the finest FHA/HUD MAP lenders in the marketplace. The LSG Lending Advisors team will review all loan documentation and walk you through the entire financing process. Schedule a call today to learn more about how we have helped so many clients with our second to none multifamily financing services.

Purchase or Refinance of Existing Multifamily Properties Insured Currently with HUD or Other Debt Sources

The HUD 223(f) program could benefit multifamily borrowers that are looking for a non-recourse, assumable, loan term up to 35 years that is fully amortizing, not to exceed 75% of the remaining economic life. This is not only an excellent solution for long term property holders, but short-term investors as well. This loan is fully assumable, subject to HUD approval, and can be very attractive to purchasers looking to acquire properties and assuming a long-term interest rate below market This feature makes a property appealing for a buyer to assume a low rate in increasing rate environments.

Maximum Loan Amount

| Market Rate |

87% Loan-to-Value |

1.15% Minimum Debt Service Coverage Ratio |

| Affordable |

90% Loan-to-Value |

1.11% Minimum Debt Service Coverage Ratio |

| 90% or Greater Rental Assistance |

90% Loan-to-Value |

1.11% Minimum Debt Service Coverage Ratio |

*Note: Loan amounts in excess of $75MM have higher Debt Service Coverage Ratio (DSCR) limits and decreased Loan-to-Value (LTV) limits.

Checkout the benefits of HUD 223(f) Transactions for Multifamily Apartments as an Infographic.

Schedule a Free Consultation Today!

Please tell us about you and your project, and someone from the LSG Lending Advisors team will reach out to you within 24-48 hours.

Frequently Asked Questions about the 223(f) Loan Program

Overview & Key Requirements of HUD 223(f) Loan

Eligible Borrowers

- Single asset, special purpose entities that are either for profit or non-profit

Eligible Properties

- Market Rate, Affordable Housing (affordable apartments for low-income families, the elderly, and people with disabilities), Unsubsidized Housing, and Subsidized Housing (HUD helps apartment owners offer reduced rents to low-income tenants);

- Properties must be at least 3 years old; and a waiver may be granted if the property is affordable and less than 3 years; and

- The property must have an average physical occupancy of 85% for 6 months prior to the loan application and maintain until close.

*Note: If there is any identity of interest between the buyer and seller in a purchase transaction, it will be considered a refinance transaction.

Amortization and Loan Term

- Maximum Loan Term up to 35 years fully amortizing, not to exceed 75% of the remaining economic life.

Cash Out

- Up to 80% LTV. 50% of cash will be released at closing, and the remaining 50% will be held in escrow until all required non-critical repairs are completed.

- A waiver can be requested to receive 75% cash at closing with 25% held in escrow until repairs are completed.

Interest Rate

- Fixed, subject to market conditions.

Commercial Space

- 223(f) 25% of net rental area and 20% of effective gross income.

Rate Lock Deposit

- 0.50% of mortgage amount collected at time of client’s acceptance of the Firm Commitment. The rate lock deposit will be fully refunded at the transaction closing.

Non-Recourse

- The HUD mortgage note will contain a non-recourse provision as to the mortgagor entity. Notwithstanding this provision, certain parties may be held personally liable to the extent of losses arising from certain “bad acts” and malfeasance, as set forth in the Regulatory Agreement. Such parties will be identified in the Firm Commitment.

Repairs/Replacements

- Repairs can’t exceed $15,536 per unit multiplied by the high cost factor for the area.

- Repairs and replacements are limited to a maximum of one major building component.

Prepayment

- 2-year lockout followed by 8 years of declining pre-pay of 8%, 7%, 6%, 5%, 4%, 3%, 2%, and 1% (other terms may be negotiated).

Assumable Mortgage

- Fully assumable, subject to HUD approval.

- This feature makes the property very appealing for a buyer to assume a low rate in increasing rate environments.

Replacement Reserves

- Annual deposits of a minimum of $250 per unit per year or higher as identified by the Physical Capital Needs Assessment (PCNA).

- An initial deposit will be required at closing which can be capitalized in the transaction and the amount is based on the PCNA.

Davis-Bacon Wage Rates

- Not applicable for this program.

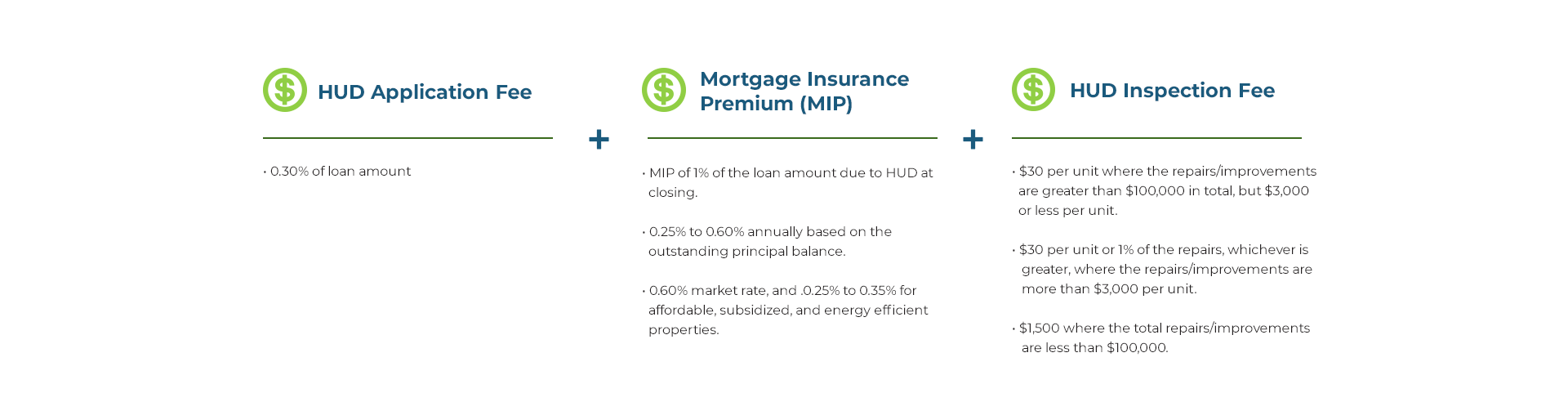

HUD Fees for 223(f) Loan

The borrower is responsible for HUD fees.

Lender Ordered Third-Party Reports for HUD 223(f) Loan

The third-party reports listed are required prior to Firm Application submitted to HUD. They are all mortgageable, and can be reimbursed from loan proceeds at closing. The amount of the reports varies depending on the size and complexity of the project.

- Appraisal

- Phase I Environmental Assessment

- Physical Capital Needs Assessment (PCNA)

*Note: Buildings constructed prior to 1978 may require lead based paint and asbestos containing material testing.

Lender Fees for HUD 223(f) Loan

A processing fee (approximately $5,000) along with the required third-party reports are collected at time of engagement with the lender.

The borrower is responsible for the costs listed below. These costs are mortgageable, and the costs vary based on the size and complexity of the transaction.

- lender financing and placement fees (up to 3.5% of the final loan amount, and payable from mortgage proceeds at closing),

- lender legal fees,

- recording fees,

- survey,

- title insurance, and

- borrower’s legal expenses.

Estimated Timeline for HUD 223(f) Loan

The average time from engagement to the closing a HUD 223(f) transaction is between 4 and 6 months.

Basic Checklist for HUD 223(f) Loan Sizing

The information listed is required for the most accurate estimate for both the loan eligibility amount and detailed estimated cost for the transaction.

HUD 223(f) Term Sheet

Download the attached Term Sheet as a reference for eligibility, Interest Rates, Requirements, Limitations, Terms and more.