The HUD 213 loans facilitate the construction, acquisition, or rehabilitation of this type of housing. Eligible projects include detached, semidetached, row, walk-up, or elevator type housing consisting of five or more units. For assistance with securing a HUD 213 loan and maneuvering through the requirements, it is critical to partner with an expert. LSG Lending Advisors has the experience to guide you and ensure a successful transaction.

- Over 7 years multifamily property loan underwriting experience.

- Expert knowledge of financial terms and principles.

- Highly experienced at guiding clients through complex transactions.

- In depth analysis of current operating statements and projected financials.

- Specialists in evaluating third party reports, including appraisals, environmental documents, market studies and project capital needs assessments.

- Loan review documentation.

- Tailor fit financing solutions for every client.

You can depend on LSG Lending Advisors to help you navigate the HUD 213 lending requirements. We don’t fund HUD loans, we guide you through them. LSG Lending Advisors advises on HUD 213 cooperative housing, FHA multifamily loans, and multifamily financing options through trusted HUD multifamily lenders. And if you have questions about this loan, LSG Lending Advisors has answers! Contact us today for a free, no obligation discussion.

Construction, Rehabilitation, or Purchase of Cooperative Housing Facilities

Mortgages financed under Section 213 of the National Housing Act are insured by the Federal Housing Administration (FHA) to facilitate the construction and rehabilitation, and purchase of cooperative housing facilities. Section 213 enables non‐profit corporations, non‐profit cooperative housing corporations, or trusts to develop housing projects to be operated as cooperatives by resident shareholders.

Overview & Key Requirements of HUD 213 Loan

Term: Up to 40 years (plus up to 36‐month construction period); Fully amortizing

Interest Rate: Fixed‐rate at commitment for both construction and permanent loans, based on market conditions and risk

Maximum Loan-To-Value: Maximum loan amount is based on the lesser of:

- 98% of HUD allowed replacement costs.

- 100% of net operating income.

- The Statutory Limit based on the type of structure and location of the project

Minimum Debt Service Coverage: 1.00x minimum for cooperative properties.

Prepayment Penalty: (typically 2‐year lockout with 8% penalty declining to 0% after year 10) No Yield Maintenance.

Non-Recourse: The mortgagor entity signs a “Section 50” certification ensuring compliance with project Regulatory Agreement.

Escrows: Replacement reserves, taxes, and insurance typically required. Working capital deposit equal to 2.0% of the mortgage amount. No operating deficit escrow is required. Sponsor must guarantee monthly charges on unsold units, and establish and maintain a General Operating Reserve account.

Third Party Reports: Market Study and Appraisal to determine rents, expenses and land value (if to be included in the HUD replacement cost total). Architecture and Cost Reviews are not needed. Borrower secures the required reports, not the lender.

Mortgage Insurance Premium: Required during construction and permanent phase. 0.70% annually; first year's premium paid at loan closing.

Eligibility:

- New construction of cooperative housing properties

- Substantial rehabilitation of projects constructed either before September 1, 1959, or constructed with Davis Bacon Wage rates

- Given that most cooperatives financed under Section 213 are age‐restricted, the head of household for buyers must be at least 62 years old

- Borrowing entity must be a non‐profit cooperative housing corporation or a non-profit corporation

- Projects must be 60% pre‐sold prior to loan closing

HUD Fees: 0.3% FHA exam fee (payable at application, may be reimbursed from mortgage proceeds)

Inspection Fees: 0.50% for new construction (payable out of mortgage proceeds)

Processing Fees: Competitive – includes cost of lender due diligence. Borrower is responsible for legal fees and standard closing costs.

Commitment Fees: Competitive and negotiable

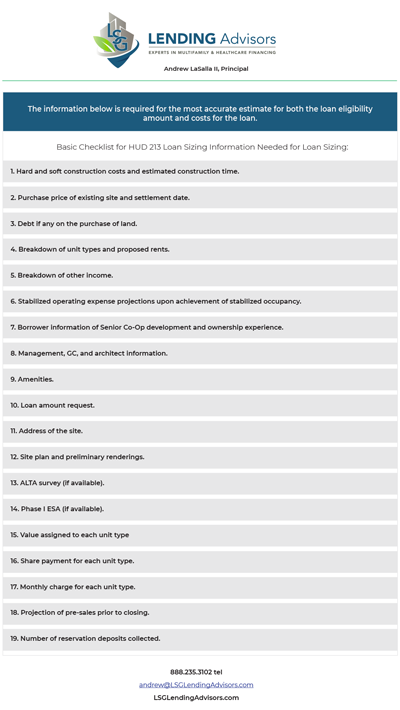

Download HUD 213 Loan Sizing PDF Checklist

Basic Checklist for HUD 213 Loan Sizing

Basic Checklist for HUD 213 Loan Sizing