HUD 221(d)(4) FHA construction loans provide long-term, fixed-rate financing for new multifamily developments. A loan advisor can guide you through the application process, qualifications, and benefits to secure optimal funding.

The FHA 221(d)(4) loan (also known as HUD 221(d)(4)) is a great financing option for those looking to develop or rehabilitate multifamily apartments.

FHA 221(d)(4) provides attractive and federally insured financing. Developers and investors can access the industry's longest-term of a fixed-rate construction loan with substantial rehabilitation financing. Terms are up to 40 years plus a 3-year construction period. Loans are non-recourse and assumable.

Navigating multifamily financing, new construction, HUD programming, and the application process can be overwhelming. We've compiled the most-asked questions for HUD 221(d)(4) to make the best use of your time.

What Do I Need to Apply for a HUD 221(d)(4)?

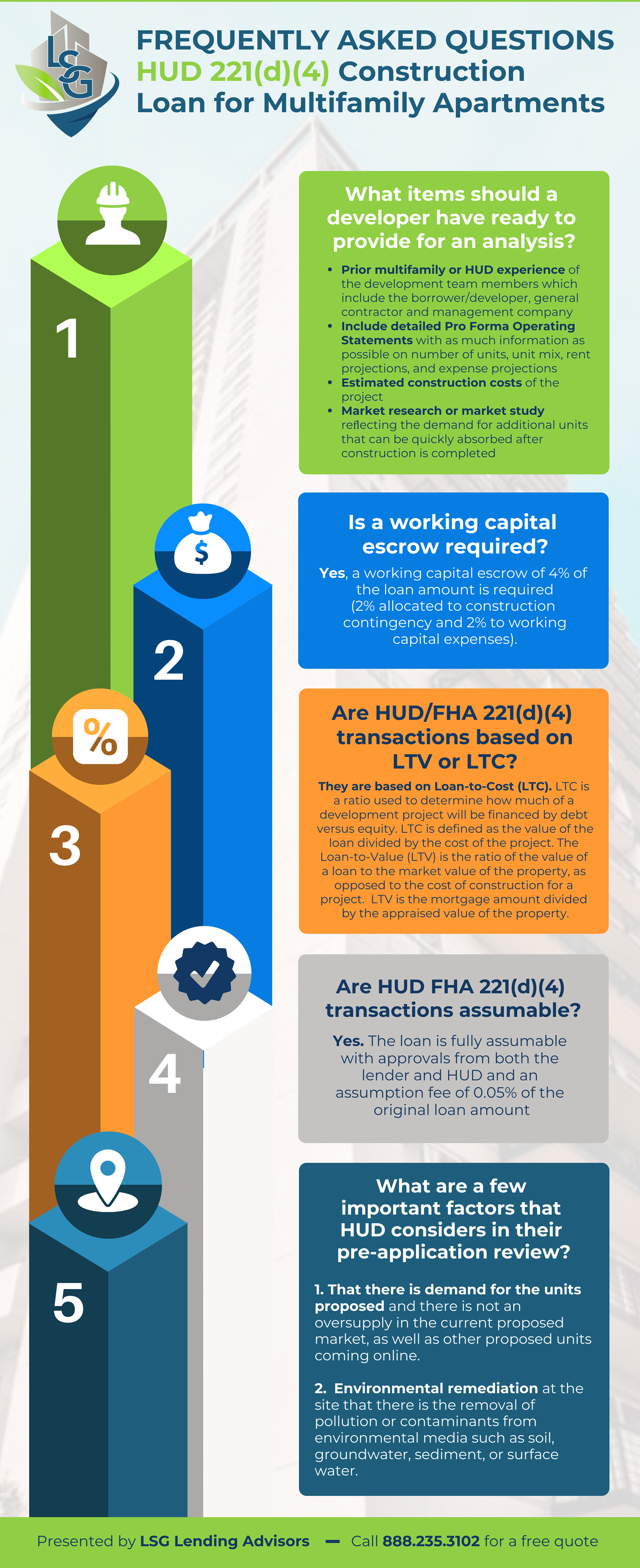

If you're interested in acquiring a FHA/HUD 221(d))4) loan, you might be wondering what kind of documentation you'll need to make your application. Be prepared with a list of eligible properties, market studies, equity requirements, and other details for an efficient process. You'll need all of the following:

1. Prior Multifamily or HUD Experience

Your development team should have experience in HUD or multifamily housing, including the borrower, developer, general contractor, and management company.

2. Include Detailed Pro Forma Operating Statements

Pro forma operating statements should be filled out with as much detailed information as possible. Be sure to include the number of units, unit mix, rent projections, and expense projections.

3. Estimate Construction Costs

The borrower or developer should provide the estimated construction costs of the project.

4. Market Research or Market Study

Market research or a market study is necessary and should be provided by the developer. Research must reflect the demand for additional units and how quickly units can be absorbed after construction is completed. 3rd party reports that the lender orders include:

- Appraisal

- Market study

- Environmental site assessment

- Architectural plan & cost review

Download the handy checklist and term sheet for HUD 221(d)(4). LSG Lending Advisors can help you through every step of the HUD 221(d)(4) construction loan process and ensure market studies, analysis, and other documents are ready.

Is a Working Capital Escrow Required?

Yes, a working capital escrow of 4% of the loan amount is required (2% allocated to construction contingency and 2% to working capital expenses).

Are HUD FHA 221(d)(4) Transactions Based on LTV or LTC?

HUD FHA 221(d)(4) is based on Loan-to-Cost (LTC). LTC is a ratio used to determine how much of a development project will be financed by debt versus equity. LTC is defined as the value of the loan divided by the cost of the project.

The Loan-to-Value (LTV) is the ratio of a loan's value to the property's market value, as opposed to the construction cost for a project. LTV is the mortgage amount divided by the appraised value of the property.

Are HUD FHA 221(d)(4) Transactions Assumable?

Yes, HUD FHA 221(d)(4) transactions are fully assumable with approvals from both the lender and HUD, along with an assumption fee of 0.05% of the original loan amount.

What Important Factors Does HUD Consider in Their Pre-Application Review?

For the pre-application review, there are two factors HUD considers essential. These include demand and remediation.

1. Demand for The Units Proposed

HUD considers there to be a demand for the proposed units and requires there not be an oversupply in the current market or if there are other proposed units coming online.

2. Environmental Remediation

Environmental remediation must be done at the site; for example, contaminants must be removed from the soil, surface water, groundwater, etc.

Contact Us Today

LSG Lending Advisors is highly experienced in HUD and FHA lending requirements. Our impressive portfolio allows us to have on hand the best, most trusted FHA and HUD-approved lenders in the industry. We can expertly navigate loan documentation, eligibility, closing, and other challenges associated with HUD 221. Contact us today to discuss HUD 221(d)(4) multifamily construction loans, transaction questions, market studies, or other concerns.